China Achieves Record $1.2 Trillion Trade Surplus in 2025 Despite Trump Tariffs as Growth Forecast Moderates to 4.5% for 2026

China posts unprecedented $1.2 trillion trade surplus for 2025 with 20% surge, defying US tariffs by pivoting to emerging markets as domestic demand challenges persist into 2026.

GLOBAL ECONOMY & TRADE

Sandeep Gawdiya

1/16/20269 min read

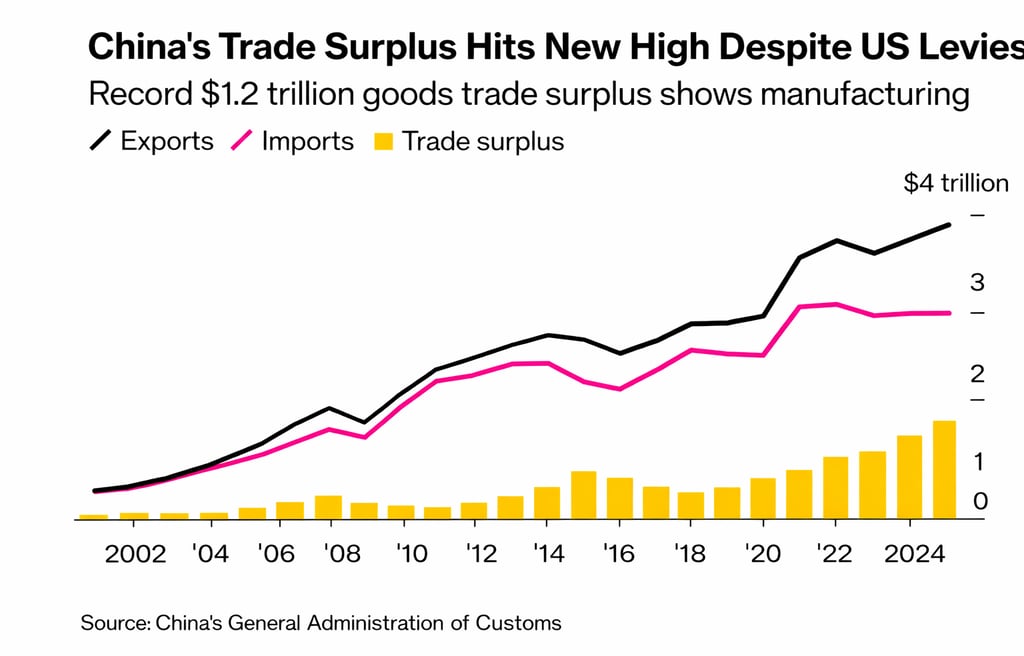

China's economy defied widespread predictions of a sharp slowdown in 2025, recording the largest trade surplus in history at $1.2 trillion despite facing the most aggressive wave of American tariffs in decades, according to official customs data released this week. The 20 percent surge from the previous year's surplus underscores how the world's second-largest economy has successfully pivoted away from its traditional dependence on U.S. consumers, forging deeper trade relationships with Southeast Asia, Latin America, Africa, and Europe to sustain its export-driven manufacturing juggernaut.

The achievement caps a year of extraordinary resilience for Chinese exporters who confronted a hostile trade environment, persistent deflationary pressures at home, and a deepening real estate crisis that has dampened domestic consumption and investment. Yet as Beijing prepares to release fourth-quarter GDP figures and 2025 annual growth data on Monday, economists warn that the export boom masks structural weaknesses that could constrain China's economic trajectory in 2026 and beyond, with growth projected to slow to 4.5 percent this year and remain at that level through 2027.

The divergent signals — surging external trade coexisting with anemic domestic demand — present Chinese policymakers with a complex challenge as they seek to rebalance the economy, boost household consumption, and navigate an international environment where President Donald Trump's return to the White House promises renewed confrontation over trade, technology, and global influence.

Export surge defies tariff pressure and shifting supply chains

According to the General Administration of Customs, China's total trade in goods reached $6.48 trillion in 2025, marking the ninth consecutive year of growth. Exports for the full year expanded 5.5 percent while imports remained essentially flat, driving the trade surplus to its unprecedented level. December alone saw exports jump 6.6 percent year-over-year, the fastest pace in three months, defying expectations for a slowdown given high comparison bases from late 2024 when businesses rushed to ship goods ahead of anticipated tariff implementations.

Wang Jun, deputy administrator of the customs bureau, told reporters at a press conference in Beijing that China "forged ahead" despite navigating a "complex and challenging external environment." He highlighted robust performance in high-tech products, with exports of advanced machinery and industrial robots rising 13 percent year-over-year. The so-called "new three" exports — electric vehicles, lithium batteries, and photovoltaic products such as solar panels — surged 27 percent, showcasing China's advancing position in critical green technology supply chains.

The geographic pattern of trade flows reveals a strategic reorientation that has accelerated under tariff pressure. China's trade with the United States, historically its largest single export market, plummeted 16.9 percent in the first eleven months of 2025 as Trump's tariff escalations — which pushed effective U.S. import tax rates on Chinese goods to levels not seen since the early 20th century — made many products uncompetitive or triggered supply chain relocations. Chinese exporters responded by dramatically expanding shipments to alternative markets, with combined increases in sales to Southeast Asia and Europe more than offsetting the American contraction.

Exports to the European Union and the Association of Southeast Asian Nations grew by 12 percent and 11 percent respectively in December, while imports from European countries jumped 18 percent, reflecting strong two-way trade relationships. Southeast Asian nations, in particular, have become critical outlets for Chinese manufactured goods as rising incomes, infrastructure improvements, and regional integration initiatives boost demand. African and Latin American markets, though starting from smaller bases, also recorded significant growth as China deepens economic ties through Belt and Road Initiative projects and commodity partnerships.

The mechanics of surplus: Supply chains, investment, and competitiveness

Analysts attribute China's export resilience to several interrelated factors beyond simple market diversification. As multinational corporations and Chinese firms relocate final assembly operations to Vietnam, Mexico, India, and other countries to avoid tariffs or satisfy "Made in" requirements, they continue sourcing components, machinery, and intermediate goods from China. This phenomenon, sometimes termed "China Plus One" or supply chain fragmentation, means that even as China's share of final product exports to the United States declines, its role as the essential supplier of industrial inputs and capital equipment expands.

The construction of factories overseas — partly driven by Chinese outbound investment — has created sustained demand for Chinese-made industrial robots, machine tools, automation systems, and production line equipment. Similarly, as countries in Southeast Asia and South Asia ramp up electronics manufacturing, they import semiconductors, displays, batteries, and precision components from Chinese suppliers who dominate global production in these categories. This upstream position in global value chains provides insulation from end-market tariffs and sustains export volumes even when geopolitical winds blow unfavorably.

China's relentless move up the value chain has also improved competitiveness and profitability in export sectors. The 13 percent growth in advanced machinery and industrial robot exports reflects technological maturation and the ability to compete with Japanese, German, and American manufacturers in sophisticated product categories. Electric vehicle exports, though facing increasing protectionist measures in Europe and elsewhere, grew from near zero a decade ago to a multi-billion-dollar business, with Chinese brands like BYD, Nio, and Geely establishing footholds in dozens of countries.

The International Monetary Fund projected China's current account surplus — which measures trade in goods and services plus investment income — at 3.3 percent of gross domestic product in 2025, one of the highest ratios among major economies. Goldman Sachs Research forecasts the surplus will rise further to 4.2 percent of GDP in 2026, well above the consensus of economist estimates at 2.5 percent, reflecting continued export strength and constrained import demand as domestic consumption remains subdued.

Domestic demand doldrums: The other side of China's economy

While exports have thrived, China's domestic economy has struggled with persistent headwinds that threaten to drag down overall growth and complicate efforts to achieve a more balanced and sustainable development model. The real estate sector, which directly and indirectly accounts for roughly a quarter of Chinese GDP, remains mired in crisis as property developers face liquidity pressures, home prices decline in most cities, and household confidence in real estate as an investment asset erodes.

Consumer spending has disappointed throughout 2025, with total retail sales of consumer goods growing just 4.5 percent year-over-year in the first three quarters, down from more robust rates in earlier years. A weak labor market, particularly for young people and those in services sectors affected by technology-driven disruption and regulatory crackdowns, has constrained household incomes and spending power. The continued fall in property values has negatively impacted the wealth effect, reducing the willingness of households to make major purchases or splurge on discretionary consumption.

Deflationary pressures have persisted despite monetary easing by the People's Bank of China. Consumer prices remained essentially stagnant in 2025, falling short of the official inflation target of around 2 percent, while producer price indices stayed negative for much of the year, reflecting overcapacity in industrial sectors and weak pricing power. Goldman Sachs Research expects producer price deflation to moderate in 2026 and turn positive in early 2027, but the prolonged period of falling or flat prices discourages investment, delays purchases, and complicates debt servicing for companies and local governments.

Beijing has responded with a series of fiscal and monetary stimulus measures, including interest rate cuts, reductions in bank reserve requirements, expanded infrastructure spending, and consumer trade-in programs offering government subsidies for replacing old appliances, vehicles, and electronics. The Central Economic Work Conference held in December 2025 identified expanding domestic demand as the top priority for economic policy in 2026, signaling leadership awareness that export-led growth alone cannot sustain long-term prosperity and social stability.

Chinese officials have pledged to "significantly" lift household consumption's share of the economy over the next five years, aiming to raise the ratio from roughly 40 percent of GDP currently to 45 percent by 2030. Most policy advisers believe this rebalancing is essential, as China's household consumption rate is about 20 percentage points below the global average while investment is roughly 20 points higher — a gap economists warn is increasingly unsustainable and represents a drag on broader industrial activity and global economic health.

Growth projections and the path ahead

Against this mixed backdrop, economists project that China's GDP growth will slow to 4.5 percent in 2026 and maintain that pace through 2027, down from an estimated 5 percent achieved in 2025. The World Bank raised its forecast for China's 2026 growth to 4.4 percent in its Global Economic Prospects report released on January 13, citing anticipated fiscal stimulus, sustained export resilience, and improved investment sentiment, while cautioning that the trajectory remains vulnerable to trade shocks and domestic financial risks.

Goldman Sachs Research holds a more optimistic view, projecting 4.8 percent growth in 2026, above the consensus estimate, based on expectations that export momentum will extend into the year and partially offset weaker domestic demand. The firm notes that export price deflation in U.S. dollar terms is expected to turn positive in 2026, rising to 0.7 percent from negative 2.7 percent in 2025, as producer price deflation moderates and the Chinese yuan appreciates slightly against the dollar.

The International Monetary Fund's updated World Economic Outlook, released on January 19, projects China's growth at 4.5 percent for 2026, with IMF Managing Director Kristalina Georgieva urging Beijing to reduce its dependence on exports and accelerate efforts to enhance domestic consumption. Eswar Prasad, a senior fellow at the Brookings Institution and former IMF China division chief, warned that China's massive trade surplus could have "destructive consequences for the global trading system alongside Trump's tariffs," as weak domestic demand suppresses imports and contributes to global imbalances.

Fourth-quarter GDP data, scheduled for release on Monday, January 20, is expected to show year-over-year growth of 4.5 percent, slightly below the third quarter's 4.8 percent, according to a Reuters poll of economists. The moderation reflects fading momentum from earlier stimulus measures and the front-loading effects that temporarily boosted activity in mid-2025. For the full year 2025, official data is expected to confirm that China met or narrowly exceeded its growth target of "around 5 percent," maintaining its position as one of the fastest-growing major economies even as structural challenges mount.

International implications and trade tensions

China's record trade surplus has significant implications for global economic dynamics and geopolitical relations. The sheer magnitude of the surplus — $1.2 trillion represents roughly 6 percent of China's GDP and is larger than the entire economies of most countries — means that vast quantities of Chinese goods continue flooding international markets, often at prices that undercut local producers and strain domestic industries in trading partners.

This export intensity is driving protectionist responses well beyond the United States. The European Union has imposed tariffs on Chinese electric vehicles, citing unfair subsidies and market distortions, and is investigating other sectors for similar measures. India, Brazil, Mexico, and Southeast Asian countries have all raised concerns about dumping and excess capacity in Chinese steel, chemicals, and consumer goods, implementing trade remedies and considering broader restrictions.

President Trump has made reducing America's trade deficit with China a central priority of his second term, threatening additional tariffs and restrictions on Chinese access to U.S. markets, technology, and investment opportunities. He recently announced that countries engaging in trade with Iran will face a new 25 percent tariff, a measure that could affect China given its economic relationship with Tehran. Such policies risk fragmenting the global trading system further and accelerating the formation of rival economic blocs centered on the U.S. and China.

Chinese officials have pushed back against characterizations of unfair trade practices, arguing that the country's export success stems from efficiency, scale, and innovation rather than subsidies or currency manipulation. They point to China's own efforts to increase imports, including commitments made in December to work toward achieving more balanced trade, though concrete policy changes have been limited and import growth has consistently lagged export expansion.

Bloomberg reported this week that China's massive trade surplus is quietly seeping into global financial markets as private Chinese businesses and individuals use their dollar earnings to purchase overseas securities and expand operations abroad. Over two trillion dollars in accumulated surpluses are being deployed into foreign assets, real estate, and business acquisitions, reflecting both investment diversification and concerns about domestic growth prospects and regulatory uncertainties.

Rebalancing imperatives: Consumption, productivity, and innovation

For China to sustain healthy long-term growth and avoid the middle-income trap that has ensnared many developing countries, economists nearly universally agree that rebalancing away from investment and exports toward consumption and services is essential. This transition requires structural reforms in areas including social welfare systems, healthcare, education, labor markets, financial sector development, and innovation ecosystems.

Expanding the social safety net — including pensions, unemployment insurance, and public healthcare — could reduce the high precautionary savings rates that Chinese households maintain and free up income for consumption. Reforming the hukou household registration system, which ties access to public services to birthplace and limits labor mobility, could help workers move to higher-productivity urban jobs and boost incomes. Financial sector liberalization and development of capital markets could improve resource allocation and support entrepreneurship and innovation.

On the supply side, China must continue moving up the value chain, shifting from low-cost manufacturing toward higher-margin products and services that leverage technological capabilities, design excellence, and brand strength. Investment in research and development, protection of intellectual property, support for startups and private enterprises, and openness to global talent and ideas are all critical to sustaining productivity growth and competitiveness in an era when traditional advantages of cheap labor and land are eroding.

The government's emphasis on "new quality productive forces" — a concept that encompasses advanced manufacturing, digital technologies, green energy, and biotechnology — reflects recognition that future growth must come from innovation rather than factor accumulation. Yet achieving this transformation while managing debt, addressing inequality, and maintaining social stability presents formidable challenges that will test the capacity and adaptability of China's economic governance system.

Conclusion: Navigating complexity and uncertainty

China's record trade surplus in 2025 tells a story of resilience, adaptability, and the enduring strength of the world's manufacturing workshop. Yet it also highlights imbalances, vulnerabilities, and tensions that complicate the country's economic future and its relationships with the rest of the world. As growth moderates toward 4.5 percent in 2026 and policymakers grapple with weak domestic demand, debt overhang, and external pressures, the path forward requires difficult choices about the pace and sequencing of reforms, the role of government versus markets, and the tradeoffs between stability and dynamism.

For the global economy, China's trajectory matters immensely. As a driver of growth, a source of supply, a market for exports, and an engine of innovation, China's performance influences everything from commodity prices to technology trends to geopolitical alignments. The coming years will test whether the world's second-largest economy can successfully navigate its transition to a new growth model, or whether structural strains and external shocks derail progress and amplify risks for all.

Updates

Delivering timely news and inspiring life stories.

Links

Contact

+917976343438

© 2025. All rights reserved.